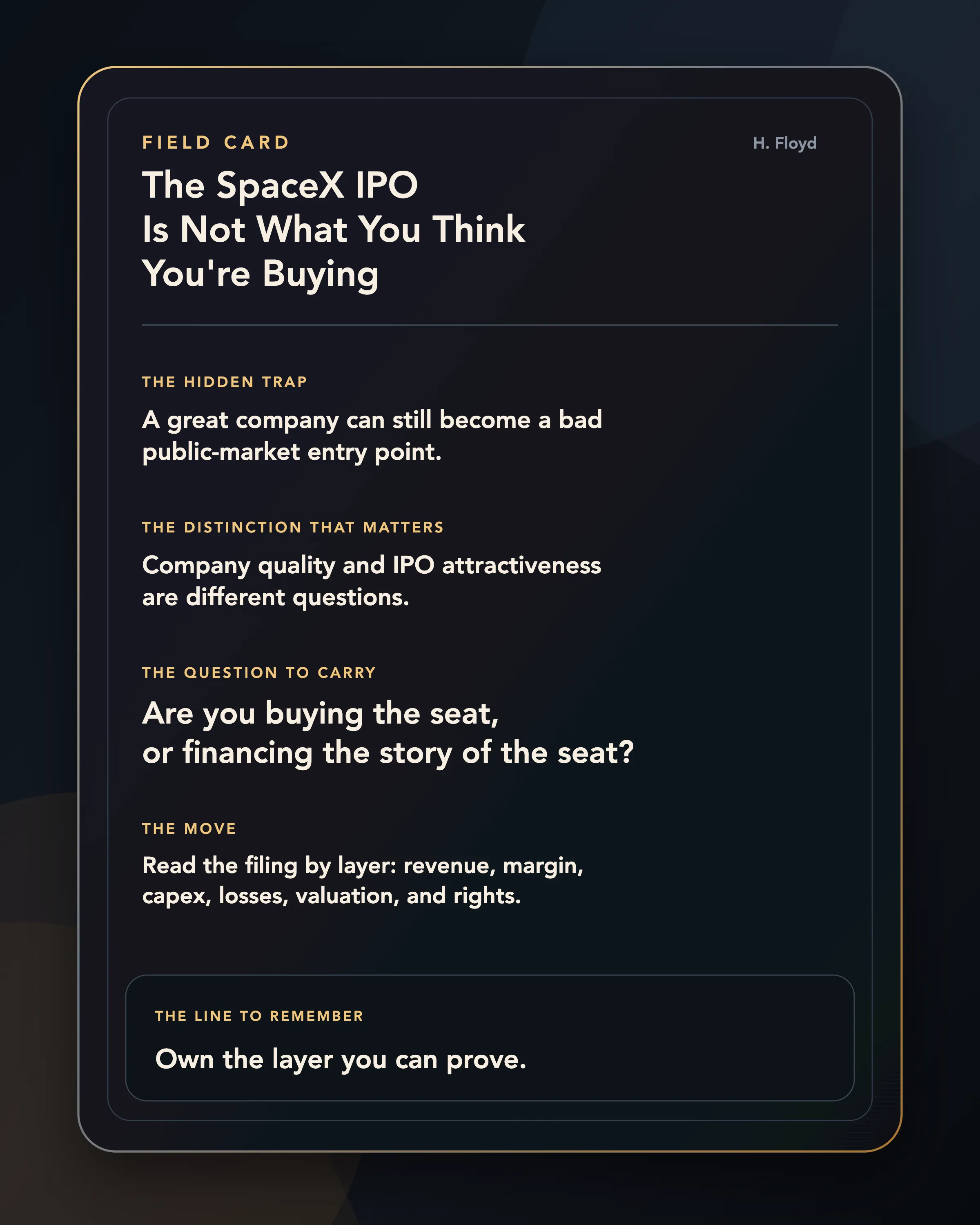

The SpaceX IPO Is Not What You Think You're Buying

The filing will not just price rockets. It will reveal which layer public investors actually own.

This is an analytical framework, not financial advice.

Reported IPO terms remain provisional until SpaceX publishes its S-1. 1

The wrong question is already forming.

It sounds sophisticated because it has a ticker-shaped answer: would you buy SpaceX?

That question is too small. It compresses too many different things into one emotional decision. It turns a complicated offering into a referendum on rockets, Elon Musk, Mars, Starlink dishes, government contracts, xAI, retail access, and the idea that the future should be investable.

The better question is stranger and more useful:

What, exactly, would you be buying?

Not just legally. Structurally.

If the reported structure holds, the offering would be more than SpaceX selling shares. It would put Starlink’s cash flows, Falcon’s industrial proof, Starship’s option value, sovereign demand, xAI’s capital appetite, Cursor’s developer-workflow distribution, orbital-compute ambition, and Musk-controlled governance into one public-market instrument.

The danger is not that investors will admire SpaceX. They should. The danger is that investors will price the bundle as if every layer is already proven, while receiving the rights of a minority passenger.

The structure is simple: Starlink earns. Starship, xAI, Cursor, and orbital compute may consume. Governance decides who benefits. Price decides whether any of it matters.

That is the lens to keep through the whole piece. This is not mainly a story about whether SpaceX is impressive. It is a story about what happens when an extraordinary private company becomes a public-market instrument. The company has an operating reality. The market has a price. The filing is the translation layer between them.

That translation is where investors get hurt.

That distinction matters because the reported SpaceX IPO would not be a normal listing. Reuters has reported that SpaceX confidentially filed for a U.S. IPO, that an early June roadshow is being targeted, and that the company could seek a valuation as high as roughly $1.75 trillion with a raise that could reach around $75 billion. 2 Reuters has also reported filing-excerpt details on Starlink economics, xAI losses, and governance. Until the prospectus is public, those are reported claims, not final terms. But even as provisional reporting, they reveal the shape of the problem.

At that scale, admiration is the easy part. The harder job is deciding which future has already been capitalised into the price.

That is the real IPO question.

Great Company, Wrong Question

Public markets are very good at turning admiration into a price. They are less good at forcing people to say which part of their admiration is already in the price.

SpaceX is not a shell with a story. It is an operating machine with proof in the world. Its official launches page, checked while building this draft, showed hundreds of completed missions, hundreds of landings, hundreds of reflights, and multiple recent Falcon missions. 3 Starlink has turned satellite internet from a niche service into a mass distribution network: Starlink’s own network update said it had more than 6 million active customers globally as of July 2025, and Reuters-sourced coverage now reports that it crossed 10 million active customers in February 2026. 4 Reuters-reported filing excerpts make the commercial point sharper: Starlink reportedly generated $11.4 billion of 2025 revenue and $4.42 billion of operating profit. 5 NASA has awarded SpaceX major Artemis Human Landing System work, including a later Option B contract modification valued at roughly $1.15 billion. 6

The hard question is whether Starlink’s cash engine is being sold as ownership, or used as collateral for Starship, xAI, Cursor, orbital compute, and founder-controlled optionality at a valuation where the future has already been monetised.

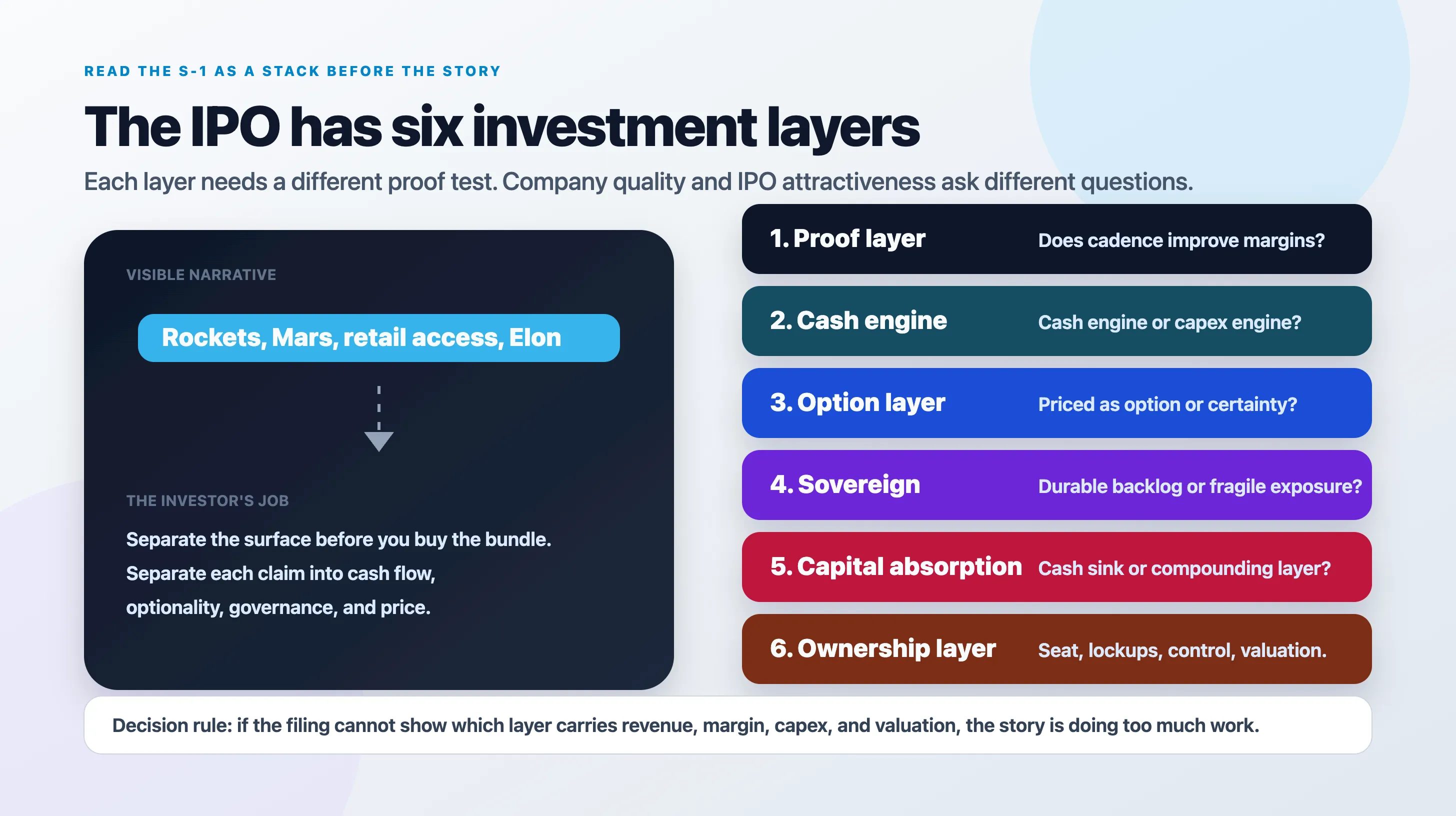

The Six Economic Layers

The cleanest way to read the offering, when it arrives, is not as one SpaceX story. It is as six layers stacked on top of each other.

1. The Proof Layer: Launch Cadence

SpaceX’s foundational achievement is not merely that it launches rockets. It is that launch has become repeatable enough to look industrial. Reusability matters because it turns a heroic event into an operating rhythm. Cadence matters because every other layer depends on it. Starlink needs launch. Government customers need reliable access. Starship needs test frequency. The narrative of orbital infrastructure needs a company that can keep putting mass into orbit while competitors are still treating launch as a sparse event.

This is the layer with the most visible proof. You can see the missions. You can see the landings. You can see the reflights. You can see the launch sites. You can see the company making launch feel less like a miracle and more like logistics.

But in an IPO, visible proof is not enough. The filing has to answer whether cadence produces operating leverage. Does each incremental mission become cheaper? Are margins improving by customer type? How concentrated is demand? How much pad, range, safety, refurbishment, insurance, and failure reserve is required to keep the machine running?

Launch cadence proves the machine. It does not prove the multiple.

2. The Cash Engine: Starlink

This may be the layer that turns SpaceX from a launch company into something closer to infrastructure. Launch gets satellites up. Starlink turns those satellites into customer relationships. That is a very different asset. A launch company sells missions. A broadband network sells recurring access. A launch company is judged by reliability and price per kilogram. A network is judged by subscribers, churn, ARPU, capacity, terminal cost, replacement capex, spectrum, enterprise mix, and distribution.

The customer number matters, but it is no longer the main uncertainty. The reported 10 million-plus customer base is enough to prove scale. The deeper question is what that scale has to fund. Reuters-reported filing excerpts say Starlink produced $11.4 billion of 2025 revenue and $4.42 billion of operating profit. That changes the burden of proof. Starlink is not merely a promising broadband project. It is, on current reporting, the cash engine inside the group.

The question is whether the engine is free to compound, or whether it is being asked to carry everything else.

That engine is real, but it is not frictionless. The Information and syndicated market reports say Starlink’s average revenue per user fell 18% to roughly $81 a month between 2023 and 2025 as the service expanded into lower-priced plans and geographies. 7 Does the network become cheaper to serve as it grows, or does each wave of growth require new satellites, new ground infrastructure, subsidised terminals, and continuous replacement spend? Does direct-to-cell become a second distribution curve, or an expensive feature? Does enterprise, maritime, aviation, and government demand protect the economics as residential pricing compresses?

The reported consolidated picture makes this sharper. Reports based on Reuters filing excerpts say SpaceX’s newly consolidated AI business posted a $6.4 billion operating loss in 2025 and consumed roughly 61% of group capex, while the combined company lost nearly $5 billion on about $18.7 billion of revenue. 8 If those numbers survive the public filing, Starlink becomes more than a growth story. It becomes the engine being asked to fund the next frontier.

Starlink is the part of SpaceX that most resembles a public-market business. The investment question is whether public holders get to own its compounding, or mainly underwrite what it is being used to finance.

3. The Option Layer: Starship

Starship is the option layer. It is the part of the story that expands the possible future more than it explains the present. If Starship works at scale, the cost and volume assumptions around orbit change. Starlink deployment changes. Lunar logistics change. Mars changes. Orbital manufacturing, propellant depots, military logistics, and large-scale cargo all move from slideware to a different sort of conversation.

But options are not cash flows. They are claims on a future state of the world.

That does not make them worthless. Some of the most valuable companies in history were underpriced because people could not value their option layers. The mistake is not valuing optionality. The mistake is paying for optionality as if it has already cleared the gates.

For Starship, the gates are unusually concrete. Test progress. Flight cadence. Regulatory approvals. Site capacity. NASA milestones. Payload commitments. Failure rates. Refurbishment assumptions. Capitalised development cost. The FAA process around Starship operations at Kennedy Space Center’s LC-39A is a reminder that the bottleneck includes licensing, environmental review, safety, range operations, and public tolerance for cadence, not engineering alone. 9 Any major Starship test near the reported roadshow window will trade as narrative evidence, not as a normal engineering update. 10

Starship is not a segment yet. It is a valuation bridge.

4. The Sovereign-Demand Layer: Government

SpaceX also sits inside national space capacity. NASA, the Space Force, national security customers, lunar missions, launch resilience, and secure communications give the company a structural role that a normal consumer-tech frame misses.

Government demand can be durable and strategic. It can also be fixed-price, milestone-heavy, politically exposed, classified, bureaucratic, and margin-constrained. A backlog headline is not enough. The filing should show contract concentration, termination rights, milestone exposure, segment margins, Starshield-style military demand, and how much of the company’s future depends on public-sector budgets. Government demand is a moat until it becomes concentration.

5. The Capital-Absorption Layer: xAI, Cursor, Orbital Compute

This is the layer most likely to produce both real upside and bad analysis, and it is now too material to leave as a vague optionality bucket.

Reuters reported that SpaceX acquired xAI in February 2026 in an all-stock transaction that valued the combined company at roughly $1.25 trillion. 11 TechCrunch and Reuters-syndicated reporting also say SpaceX has announced a Cursor arrangement: either a $10 billion partnership payment or an option to acquire the coding and knowledge-work AI company for $60 billion later in 2026. 12 Separate reporting says SpaceX has sought regulatory review for orbital AI/data-centre satellite plans. 13

Those claims are not all equal. The xAI transaction is a Reuters-reported corporate event. The Cursor arrangement has a public statement and press coverage, but the detailed terms are still thin. The orbital compute ambition is a regulatory-and-strategy claim, not an operating business. Still, together they change the analytical frame.

The Musk ecosystem has moved from adjacency to possible issuer-level risk. The bullish version is that SpaceX becomes the physical layer for AI: launch puts infrastructure in orbit, Starlink distributes connectivity, xAI supplies models and compute, Cursor supplies developer workflow distribution, and Tesla may provide storage or energy adjacency.

It is also exactly the kind of thesis that can become unfalsifiable if investors let it float above the accounts.

If xAI, Cursor, orbital compute, or broader AI infrastructure is part of the SpaceX story, the public filing must tell investors what they actually own. Is xAI consolidated? How much loss and capex comes with it? Are there related-party transactions with Tesla, X, or other Musk-controlled entities? Who funds the compute build-out? What assets sit in which entity? What are the Cursor payment and acquisition obligations? What governance rights protect outside shareholders? Are capital allocation decisions made for SpaceX shareholders, or for the ecosystem as a whole?

The Cursor point is a good example. Strategically, a coding and knowledge-work AI layer could produce real engineering-productivity gains inside the rocket and satellite programmes. It could also be exactly the kind of late-cycle narrative expansion public investors should interrogate: expensive, adjacent, exciting, and not yet proven as a return stream.

AI optionality should not be dismissed. But optionality without legal and accounting clarity is not a thesis. It is a mist. The bear case is not that AI is irrelevant. It is that Starlink’s cash flows are redirected into an AI capex race with unclear returns.

6. The Ownership Layer: Governance, Liquidity, Price

This is the layer that enthusiastic investors least want to discuss, and the one that may matter most.

A historic IPO would create a new public liquid instrument for one of the most desired private companies in the world. That liquidity has value. It also has danger. Retail access can democratise participation, but it can also turn scarcity into demand pressure. If a large retail allocation is part of the offering, as Reuters has reported, the investor has to ask whether retail is being invited into a durable seat or into a narrative event.

Governance is not a footnote here. It is the mechanism by which public investors find out whether they are owners, passengers, or liquidity providers.

Reuters-syndicated reports on filing excerpts point to a dual-class structure in which public investors buy lower-vote Class A shares while Musk and insiders retain super-voting Class B control, with some reports putting Musk at roughly 42% economic ownership and about 79% voting control. 14 Treat those exact percentages as provisional until the prospectus is public. Treat the direction as central.

Reuters-syndicated reporting also says the filing language would make Musk removable from board or top roles only by Class B holders, while a proposed compensation package could grant large additional super-voting awards tied to extreme Mars and orbital-compute milestones. 15

The governance point does not need exaggeration. If the reported structure holds, public shareholders would be buying into one of the most ambitious companies in the world while accepting unusually limited control over how that ambition is directed. Control is not incidental to this IPO. It is one of the assets being sold around.

Share classes, voting control, lockups, insider sales, related-party rules, use of proceeds, segment disclosure, and risk-factor language are not footnotes here. They are the ownership terms. The company can be extraordinary and still offer public investors weak rights at a demanding price.

Governance determines whether public investors are buying ownership or exposure.

What The Proceeds Actually Buy

The reported $75 billion raise should not be read as generic rocket money. At this scale, the IPO is a capital-allocation document.

The use-of-proceeds section will show whether public investors are funding Starship cadence, Starlink capacity, AI compute, orbital data-centre ambition, debt reduction, insider liquidity, or some mixture of all of them. Reported filing excerpts already flag orbital data-centre plans while warning that they may not become commercially viable.

If the proceeds strengthen the operating substrate, public investors may be buying into a seat that compounds. If they mainly finance losses, related-party complexity, or narrative expansion ahead of proof, they are underwriting the next layer of the story.

This is why the use-of-proceeds section may be one of the most important pages in the filing.

The Reference Class Trap

The valuation debate will look quantitative. It will be full of numbers, multiples, curves, comps, TAMs, backlogs, and scenario cases.

Underneath those numbers will be one hidden decision: compared to what?

If you compare SpaceX to launch providers, the valuation will look impossible. If you compare it to telecom infrastructure, it will depend on Starlink’s margins and replacement capex. If you compare it to defence primes, you will care about government backlog, political risk, and free cash flow durability. If you compare it to mega-cap platforms, you will focus on ecosystem control and the ability to compound across layers. If you compare it to AI infrastructure, you will care about compute, power, software distribution, and capex absorption. Reuters reported that bankers and investors have been reaching for Palantir, GE Vernova, and Vertiv-style AI infrastructure comparisons rather than Boeing or telecom comps. 16 Damodaran’s pre-prospectus valuation work reached a base case around $1.22 trillion and a simulation median around $1.29 trillion, while noting that $1.75 trillion to $2 trillion pricing leaves little obvious upside for a new buyer. 17

That spread is not a trivia point. It is the whole psychological game. The same facts can look cheap or expensive depending on which future you let into the denominator.

The reference class is not a neutral choice. It is the move that makes the valuation possible.

None of those reference classes is obviously right.

That is the point.

The biggest analytical error will be choosing the flattering reference class implicitly. SpaceX will be called an infrastructure company when people want durability, a technology company when people want growth, a defence asset when people want sovereign importance, a telecom company when people want recurring revenue, an AI company when people want multiple expansion, an “AWS in space” when people want platform economics, and a founder-led compounder when people want to explain away governance.

The S-1 should be read as a reference-class document.

Not because the reference class is an academic detail. Because the reference class quietly decides what future you are paying for.

Which business actually carries revenue?

Which business carries margin?

Which business carries capex?

Which business carries the valuation?

Those may not be the same business.

The Part Investors Will Be Tempted To Skip

There is a specific kind of company where scepticism feels small. SpaceX is one of them.

The accomplishments are so visible that ordinary caution can look like a failure of imagination. The rockets land. The satellites work. The launch cadence is real. The government trusts the company with missions that matter. Starlink has millions of customers. Starship could change the cost curve of orbit. The founder has already made several impossible-looking markets real.

All true. But investing does not reward awe. It rewards the relationship between price, rights, cash flows, growth, risk, and time.

At one valuation, SpaceX might be Starlink cash flow with free Starship optionality. At another, it becomes Starlink cash flow plus paid Starship optionality. At the reported IPO range, it may become a bet that launch, Starlink, Starship, government demand, xAI, Cursor, orbital compute, Mars, and retail scarcity all work, and that public investors still receive enough economics after the structure is defined.

Same company. Different investment.

The Six Questions That Matter

When the filing appears, do not start with the valuation.

Start with six questions:

-

Which segment carries revenue?

-

Which segment carries margin?

-

Which segment carries capex?

-

Which segment carries losses?

-

Which segment carries the valuation?

-

What rights do public shareholders actually receive?

Then read the details underneath those questions. Launch cadence proves capability, not valuation. Starlink should show whether it is a cash engine after constellation maintenance. Starship should show whether it is priced as an option or a certainty. Government demand should show whether durability is becoming concentration. xAI, Cursor, and orbital compute should show whether public shareholders own the upside or merely fund the spend. Governance should show whether public investors are owners, passengers, or liquidity providers.

Only then ask the price question.

What Would Change The Answer

The bullish version is not hard to imagine.

The filing shows Starlink converting scale into strong free cash flow after replacement capex. Launch margins improve with cadence. Starship risk is disclosed clearly but not carrying the whole valuation. Government backlog is durable without becoming the only profit pool. xAI losses are large but bounded, Cursor is tied to real engineering-productivity gains inside the rocket and satellite programmes, related-party boundaries are clean, and AI capex has a visible route to revenue. Governance is founder-controlled but not abusive. Use of proceeds strengthens the operating substrate. The valuation is demanding but not so demanding that every future layer must work perfectly.

That would be a serious public-market asset.

The bearish version is also not hard to imagine.

The filing reveals that Starlink growth is capex-hungry after replacement spend, launch cadence is operationally heroic but financially thinner than assumed, Starship is essential to the valuation but still distant from commercial proof, government demand is milestone-risky or politically concentrated, xAI losses widen, Cursor becomes another expensive option, related-party complexity muddies the economics, insiders sell into retail demand, and the valuation already prices every option as if it were a proven segment.

That would still be an extraordinary company.

It might not be an attractive IPO.

This is the distinction the public conversation will try to erase. Keep it alive.

The Real Thing Being Sold

The obvious story is rockets.

The more sophisticated story is Starlink.

The grand story is Mars.

The market story is scarcity: a company everyone has heard of, few have been able to own, and many will want the moment it becomes available.

But the structural story is different.

SpaceX may be selling public investors access to a seat in the orbital economy. Not a single product, but a position: launch, satellites, communications, government access, Starship capacity, AI compute, developer workflow, maybe a new layer of physical distribution above the planet.

That is why the company matters.

It is also why the IPO could be dangerous.

The best seats are accumulated slowly and priced imperfectly before the world understands them. By the time everyone recognises the seat, the price may already include the seat and every future use of it.

So when the SpaceX filing arrives, the question is not whether the company is impressive. That part is obvious.

The question is whether public investors are being offered the seat, or being asked to finance the story of the seat at a price that assumes every future use of it has already been won.

That is the IPO question.

If you take one habit from this piece, make it this: when a story feels obviously great, slow down and ask what part of the machine you can actually prove.

I wrote about the same test in public markets in PLTR: The AI Stock That Has To Prove It Owns The Permission Layer, and from the operator side in AI Made You Faster. It Did Not Make You Safer.. Both are really about the same thing: do not confuse exposure with ownership, or speed with proof.

If the SpaceX filing lands and you read it, I would love to know which layer looks most proven to you, and which layer looks most like story.

Field Card

No public SpaceX S-1 or prospectus was available during the May 5 pre-publication check. That is why the article treats Reuters-reported filing excerpts as provisional and points readers back to the eventual prospectus as the document that should settle the terms.

Reuters reported that SpaceX had confidentially filed for a U.S. IPO, was targeting an early June roadshow, and could seek a valuation around $1.75 trillion with a raise of up to roughly $75 billion. Those figures remain reported terms until a public prospectus is available: https://www.reuters.com/business/spacex-lays-out-ipo-details-targets-early-june-roadshow-sources-say-2026-04-07/

SpaceX’s official launch record is the source for completed missions, landings, reflights, and recent Falcon activity: https://www.spacex.com/launches/

Starlink said it had more than 6 million active customers globally as of July 2025. Reuters-sourced market coverage later reported that Starlink crossed 10 million active customers in February 2026: https://www.starlink.com/networkupdate and https://finance.yahoo.com/markets/stocks/articles/starlink-user-growth-accelerates-spacex-134543171.html

Reuters-reported filing excerpts are the source for the Starlink 2025 revenue and operating-profit figures cited in the piece: https://reuters.com/science/spacex-posted-nearly-5-billion-loss-2025-information-reports-2026-04-10

NASA’s Artemis Human Landing System Option B modification is the source for the roughly $1.15 billion contract figure: https://www.nasa.gov/press-release/nasa-awards-spacex-second-contract-option-for-artemis-moon-landing-0/

The Information / syndicated market reporting is the source for the reported 18% fall in Starlink ARPU to about $81 between 2023 and 2025: https://sa.marketscreener.com/news/spacex-says-starlink-s-arpu-fell-18-to-81-to-keep-falling-the-information-ce7f58dadc88ff20

Reuters-syndicated reporting on filing excerpts is the source for the reported consolidated revenue, loss, xAI operating loss, and capex-share figures: https://ca.finance.yahoo.com/news/exclusive-spacex-conquered-stars-now-100320149.html

FAA Starship-Super Heavy materials for LC-39A show why Starship cadence is partly a licensing, safety, environmental, and range-operations question, not only an engineering question: https://www.faa.gov/space/stakeholder_engagement/spacex_starship_ksc

NASASpaceFlight reported Starship Flight 12 static-fire activity and a possible mid-May target window. This matters here because a visible test near a roadshow can influence narrative, even before it proves commercial economics: https://www.nasaspaceflight.com/2026/05/spacex-mid-may-starship-flight-12-revised-trajectory/

Reuters reported the SpaceX-xAI all-stock transaction and the reported combined valuation: https://www.reuters.com/business/musks-spacex-merge-with-xai-combined-valuation-125-trillion-bloomberg-news-2026-02-02/

TechCrunch reported the Cursor arrangement, including the partnership payment and later acquisition option described in the piece: https://techcrunch.com/2026/04/21/spacex-is-working-with-cursor-and-has-an-option-to-buy-the-startup-for-60-billion/

TechCrunch reported SpaceX’s orbital AI/data-centre satellite filing. The article treats this as a strategic ambition and regulatory request, not approved commercial capacity: https://techcrunch.com/2026/01/31/spacex-seeks-federal-approval-to-launch-1-million-solar-powered-satellite-data-centers/

Reuters-syndicated reporting on filing excerpts is the source for the reported Class A/Class B governance structure and provisional Musk voting-control figures: https://finance.yahoo.com/markets/stocks/articles/exclusive-musk-insiders-retain-voting-065827904.html

Reuters-syndicated reporting is the source for the described Musk compensation package tied to Mars and orbital-compute milestones: https://ca.finance.yahoo.com/news/analysis-spacex-ties-musk-compensation-100426004.html

Reuters / Investing.com reported that bankers and investors were reaching for Palantir, GE Vernova, and Vertiv-style AI-infrastructure comparisons when discussing SpaceX’s reported valuation: https://ca.investing.com/news/stock-market-news/the-unconventional-logic-behind-spacexs-175-trillion-price-tag-4558854

Aswath Damodaran’s April 2026 SpaceX valuation piece is the source for the base-case and simulation-median valuation references: https://open.substack.com/pub/aswathdamodaran/p/to-trillions-and-beyond-a-spacex

If a single argument here changed what you were about to trust, the highest-leverage move is to subscribe on Substack. One piece a week, no filler.