PLTR: The AI Stock That Has To Prove It Owns The Permission Layer

A bull/bear thesis for Palantir: not whether AI demand is real, but whether Palantir owns the permission layer between model capability and real-world action.

Research frame, not investment advice.

Palantir is easy to write badly.

The bull version becomes a cheerleading note: AI is huge, Palantir is growing fast, governments trust it, enterprises are buying AIP, and the margins look like elite software.

The bear version becomes a valuation complaint: the stock is wildly expensive, the story is crowded, insiders sell, and the price already assumes something close to perfection.

Both versions miss the harder question.

The real PLTR debate is not whether Palantir is riding the AI cycle. That frame is too blunt to be useful.

The better question is:

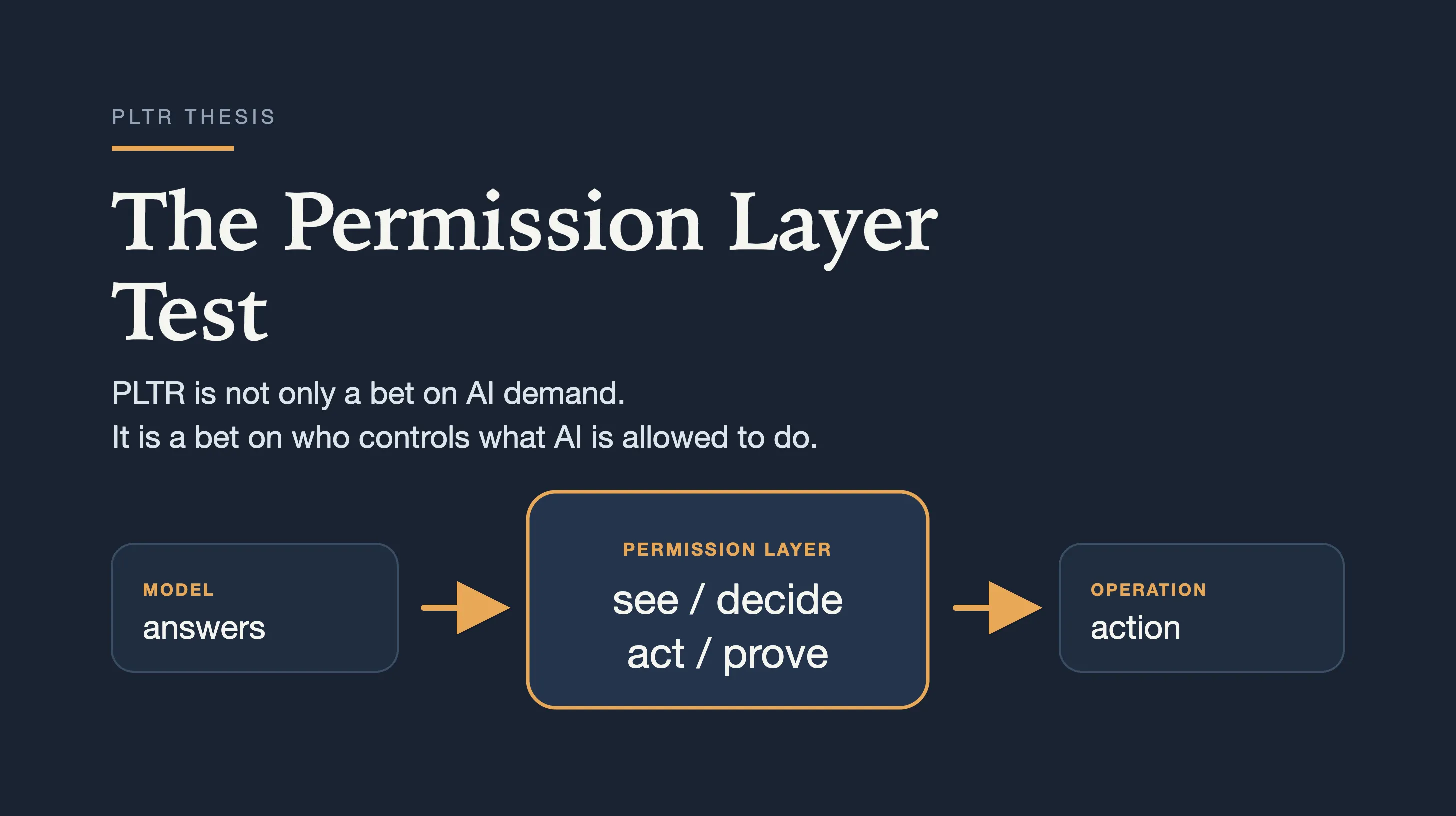

When AI moves from demos into real organisations, who owns the layer that decides what the system is allowed to see, decide, do, and prove afterwards?

That is the permission layer.

And that is what Palantir has to prove it owns.

The distinction changes how you look at the company. A model can answer a question. A workflow can move work forward. But a permission layer decides whether an AI system is allowed to touch what matters: operational data, regulated decisions, live actions, and evidence that can survive audit.

This is why Palantir is interesting. Not because it is another beneficiary of AI spending, but because it may sit at the point where AI spending becomes operationally real.

A story can be true and still be over-owned. An instrument becomes harder to replace the more the world depends on the thing it measures, controls, or makes executable.

PLTR is the argument between those two sentences.

The useful question is not whether AI is useful. It is who controls the path from model capability to real-world action.

The Thesis In One Sentence

Palantir is a bet that the bottleneck in AI deployment moves from model capability to permissioned execution: the ability to make AI see the right context, target the right action, obey the right constraints, and leave behind proof.

That sentence is doing a lot of work, so let me unpack it.

The public AI conversation still treats intelligence as the scarce layer. Which model is smartest? Which benchmark moved? Which chatbot can reason better?

Regulated enterprises and governments do not live in that world for long.

They do not only need a model that can produce an answer. They need a system that knows which data the model can see, which action it can take, which human must approve it, which trace gets preserved, and which decision can be defended later.

That gives us a more useful way to judge Palantir than the usual AI-stock framing.

Ask four questions:

-

See: can the system connect to the organisation’s real data, not a cleaned-up demo version?

-

Decide: can it target the right operational choice, not just produce a plausible answer?

-

Act: can it execute inside permissioned workflows without blowing through constraints?

-

Prove: can it preserve the evidence trail when someone asks what happened?

That is the Palantir test:

Can Palantir own the loop between data, decisions, actions, and proof?

If Palantir owns that loop, the company is not just selling AI software. It is selling operational control.

If Palantir does not own that loop, then it is a very impressive software company trading like it owns more of the future than it actually does.

The underlying idea is simple: powerful AI inside a messy organisation is not automatically useful. It becomes useful only when the organisation can see the right context, aim the system at the right target, constrain what it is allowed to do, and prove what happened afterwards.

That is the part Palantir is trying to own.

Reader map: if you remember one thing, remember the split between useful AI and allowed-to-act AI. Palantir’s valuation only makes sense if that second layer stays scarce.

What The Market Is Already Paying For

The market is not asleep to this possibility.

Palantir’s own Q4 2025 release gives the bull case real numbers to work with: 1

-

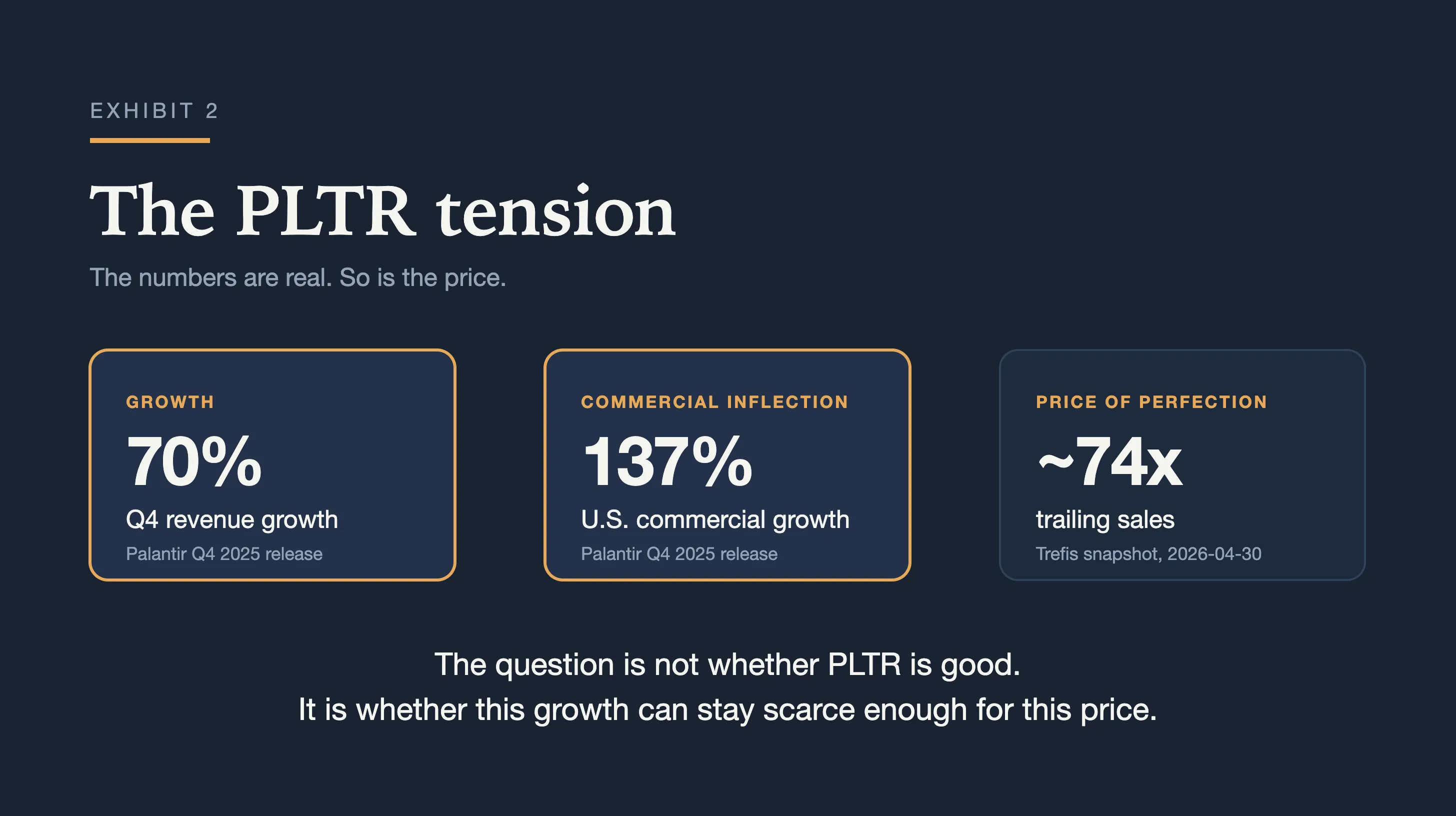

FY 2025 revenue: $4.475 billion, up 56% year over year.

-

Q4 2025 revenue: $1.407 billion, up 70% year over year.

-

U.S. commercial revenue in Q4: $507 million, up 137% year over year.

-

U.S. government revenue in Q4: $570 million, up 66% year over year.

-

FY 2026 revenue guide: $7.182-$7.198 billion, implying about 61% growth.

-

FY 2026 U.S. commercial revenue guide: more than $3.144 billion, implying at least 115% growth.

-

Adjusted free cash flow margin in Q4: 56%.

These are not hype numbers. They force a serious bear to work harder.

But the price is doing work too.

At roughly $332 billion of market value and about 74 times trailing sales as of the Apr 30 Trefis snapshot, the stock is not merely pricing in a good software business. It is pricing in a business that stays scarce while the rest of the AI stack commoditises around it. 2

The market is already underwriting a specific future:

-

AI use keeps moving from pilots into live operations.

-

Regulated customers need more than generic model access.

-

Palantir remains one of the few credible vendors for that deployment layer.

-

Commercial adoption keeps accelerating without destroying margins.

-

Hyperscalers do not bundle away enough of the workflow, audit, and permissioning layer to compress the premium.

That is a lot to ask.

The stock is not asking whether Palantir can be good. It is asking whether Palantir can remain exceptional for long enough that today’s valuation becomes a rational underwriting rather than a momentum receipt.

This is why PLTR is a useful test case. The company is producing the kind of growth that deserves attention. The price is asking whether that growth belongs to a scarce layer, not just to an AI budget cycle.

The Bull Case: Palantir Owns A Scarce Layer

The strongest bull case is not “AI is big.” That is too broad. It explains almost nothing.

The stronger bull case is that Palantir sits where generic AI stops being useful and operational AI starts being valuable.

There is a canyon between “this model can answer a question” and “this system can run a live decision inside a hospital, factory, bank, battlefield, or government agency.”

A large company does not become AI-native because someone plugs an LLM into Slack. A government agency does not modernise because a chatbot can summarise a PDF. The hard part is connecting messy data, permissions, workflows, decisions, and audit trails into a system that can survive contact with operations.

This is where Palantir’s ontology language matters. The word can sound abstract, but the practical claim is simple: Palantir tries to model how an organisation actually works.

Which objects matter? Which relationships matter? Which users can act on which information? Which decisions need to be made at which point in the process? Which actions require a human? Which outputs need a trace?

If that model becomes embedded inside the customer, the moat is not only software. It is context.

This is the deeper point: architecture often outlives content. The models will change. The workflows will change. The specific AI interface will change. But if the organisation’s operational map lives in Palantir, the scaffold may persist while the content turns over.

This is also why the government side matters. Defence, intelligence, and regulated operations are not ideal environments for generic AI wrappers. They need permissioning, provenance, escalation, and traceability. They need systems that know not just what can be generated, but what can be done.

The bull case is that AIP has turned this old Palantir strength into a faster commercial motion.

The numbers support that possibility. U.S. commercial revenue grew 137% year over year in Q4 2025. U.S. commercial remaining deal value reached $4.38 billion, up 145% year over year. Total contract value in Q4 was $4.262 billion, up 138% year over year. 3

If those numbers represent durable platform adoption rather than a temporary AI budget surge, PLTR becomes one of the cleanest public-market examples of a bigger shift: companies paying for the systems that let AI act safely, not just answer fluently.

The bull case, stated cleanly, is this:

As model intelligence becomes more available, the scarce layer becomes the system of permissioned execution around it. Palantir may already be installed where that scarcity appears first.

That is a strong case. It is also exactly why the bear case has to be better than “the stock is expensive.”

The Bear Case: The Thesis May Be Right And The Stock Still Too Expensive

The weak bear case is that Palantir is overhyped.

That is not good enough.

A better bear case starts by granting the company its strengths. Palantir may be a rare business. The product may be real. AIP may be accelerating adoption. The government moat may be durable. The margins may be excellent.

A great company can still be a bad underwriting if the market has already bought the whole story.

A company trading at more than 70 times sales does not merely need to grow. It needs to keep the market believing that its growth is unusually durable, unusually profitable, and unusually hard to compete away.

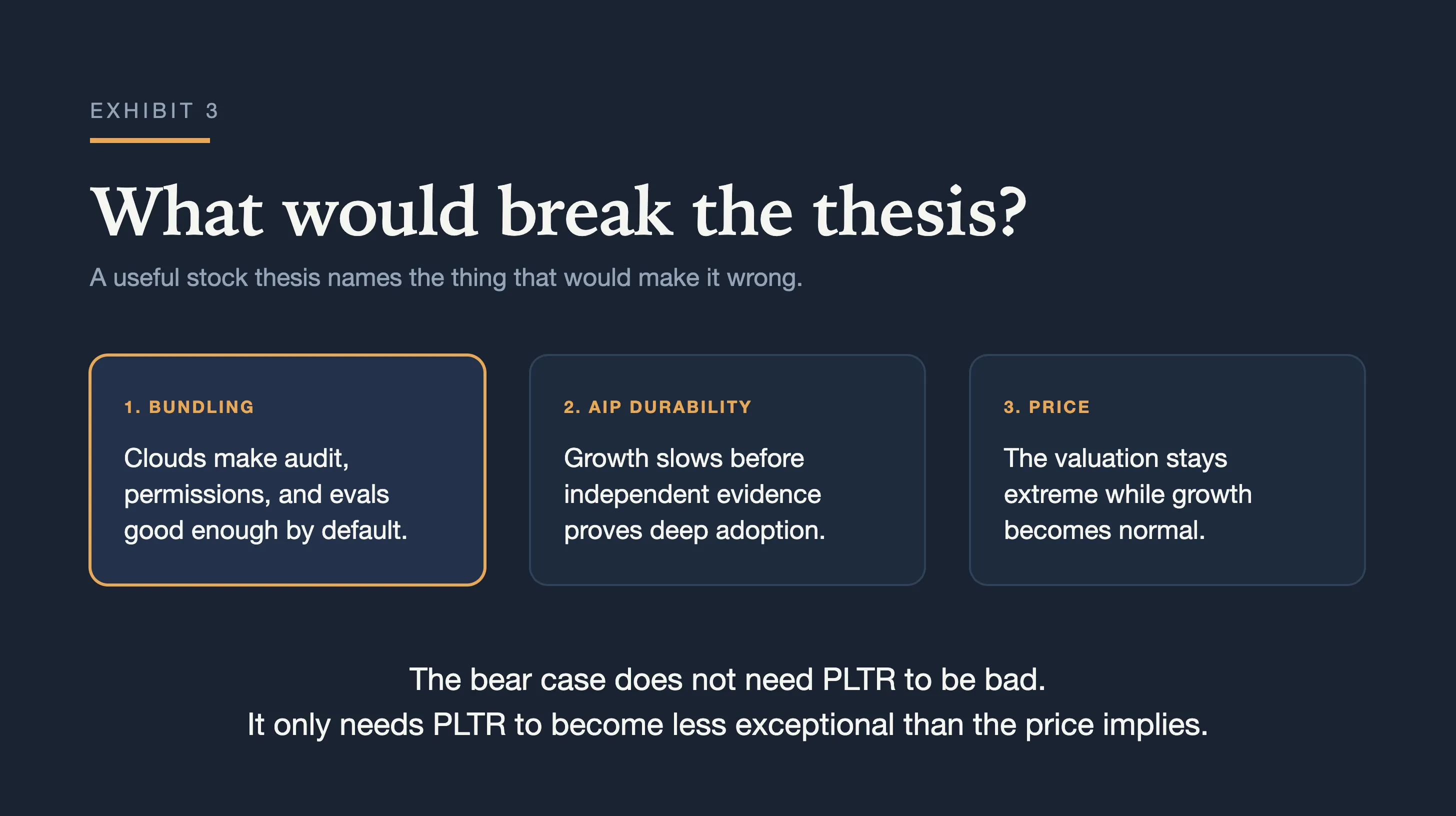

Several things can break that belief.

First, hyperscalers can bundle enough of the instrument layer into the cloud stack. If Azure, Google Cloud, AWS, OpenAI, or Anthropic make AI governance, evals, audit trails, and permissioning good enough inside their own platforms, some customers may accept the bundled version rather than paying a Palantir premium.

Second, AIP traction is still partly company-reported. The growth is real, but commercial AIP durability is not yet independently triangulated enough to treat every bootcamp, customer count, or deal metric as proof of deep production embedding.

Third, government strength cuts both ways. It validates the product in demanding environments, but it also introduces procurement cycles, political risk, budget exposure, and reputational constraints.

Fourth, the valuation makes every slowdown louder. If revenue growth normalises before margins and customer expansion prove the full platform thesis, the multiple can compress even while the business keeps improving.

That is the uncomfortable part of PLTR: the bear case does not require the company to disappoint in an ordinary sense.

It only requires the company to become less exceptional than the price implies.

The bear case is not that the story is fake. The bear case is that the story is so attractive that the market may have stopped asking what would falsify it.

That makes PLTR a useful mental model for AI investing more broadly: who owns a scarce control point after model capability gets cheaper?

If the answer is “Palantir owns the permission layer,” the premium may have logic.

If the answer is “Palantir is one strong vendor inside a layer that clouds, model labs, and internal platforms can partially absorb,” the premium becomes much harder to defend.

What Would Change My Mind

The point of a bull/bear article is not to sound balanced. It is to make the thesis falsifiable.

For PLTR, I would watch four things.

1. Bundled AI governance gets good enough

If hyperscalers bundle eval, audit, observability, permissions, and model governance into the model or cloud API at low incremental cost, Palantir’s instrument-layer scarcity weakens.

This does not require hyperscalers to replicate Palantir completely. They only need to be good enough for enough customers.

2. AIP growth slows before durability is proven

If U.S. commercial growth slows sharply before there is independent evidence that customers are building durable operational workflows on AIP, the market may reclassify AIP from platform shift to adoption spike.

3. Verification depth does not become a priced contract dimension

The right listen-for is whether Palantir can price verification depth. Sampling, replay coverage, trace retention, judge configuration, audit bundles, permission ladders, and regulated workflow evidence are the kinds of features that would make the thesis concrete.

If customers pay for those layers, the thesis strengthens.

If they treat them as bundled table stakes, the thesis weakens.

This is subtle but important. A feature can be necessary without being separately valuable. Palantir needs the market to pay for the depth of the instrument, not merely expect it as part of the package.

4. Valuation stays extreme while growth normalises

This is the simplest one.

Great company, bad underwriting.

If growth normalises and the stock still trades as though the exceptional phase is permanent, the risk shifts from business quality to entry price.

Verdict

PLTR is one of the most interesting public-equity expressions of the AI-deployment thesis.

It is not just an “AI stock.” It is a bet on the layer that makes AI usable inside organisations where mistakes matter.

More specifically, it is a bet that the money in enterprise AI moves toward permissioned execution: see the right data, decide against the right target, act inside the right constraints, and prove what happened afterwards.

That is a much better lens than “AI beneficiary.”

It also makes the valuation harder, not easier. The stock is already priced like the market understands a lot of this.

So my current posture would be:

Watchlist / research, not automatic buy.

The company may be exceptional. The article’s job is not to deny that.

The job is to separate three things that often get collapsed:

-

Is the business real?

-

Is the moat durable?

-

Is the current price a good underwriting of that durability?

For Palantir, the answer to the first is increasingly yes.

The second is the live thesis: does Palantir really own the permission layer, or does it only participate in it?

The third is where the fight is.

If you want more pieces like this, subscribe for essays on AI, markets, and the hidden infrastructure layer behind what looks like hype.

Palantir Q4 2025 earnings release / SEC Exhibit 99.1, including FY 2025 revenue, Q4 2025 segment growth, FY 2026 guidance, free-cash-flow margin, total contract value, and U.S. commercial remaining deal value: https://www.sec.gov/Archives/edgar/data/1321655/000132165526000004/a2025q4ex991earningsrelease.htm

Trefis PLTR valuation snapshot used for the Apr 30 market-cap and valuation-multiple references. https://www.trefis.com/data/companies/PLTR?from=PLTR-2026-03-01

Palantir Q4 2025 earnings release / SEC Exhibit 99.1, including FY 2025 revenue, Q4 2025 segment growth, FY 2026 guidance, free-cash-flow margin, total contract value, and U.S. commercial remaining deal value: https://www.sec.gov/Archives/edgar/data/1321655/000132165526000004/a2025q4ex991earningsrelease.htm

If a single argument here changed what you were about to trust, the highest-leverage move is to subscribe on Substack. One piece a week, no filler.